Published: 28 January 2026

The introduction of UAE Corporate Tax marks a major shift in the country’s tax landscape. Long known for its tax-friendly environment, the UAE now levies corporate tax on business profits under Federal Decree-Law No. 47 of 2022.

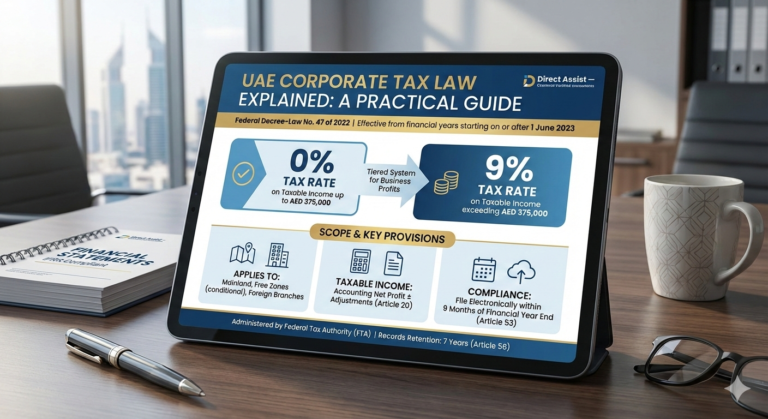

The law applies to financial years starting on or after 1 June 2023 and establishes a clear framework for how businesses calculate, report, and pay corporate tax.

At Direct Assist, we help UAE and international businesses understand their obligations and remain compliant while planning efficiently. This guide breaks down the key provisions of the UAE Corporate Tax Law in plain English.

UAE Corporate Tax is a direct federal tax imposed on the net profits of businesses operating in the UAE.

It applies uniformly across all seven emirates and is administered by the Federal Tax Authority (FTA).

Corporate Tax applies throughout the UAE, including:

Mainland businesses

Free Zone entities (subject to conditions)

Branches of foreign companies

As a federal tax, it replaces the historic emirate-level tax regimes that were largely inactive.

The UAE introduced corporate tax to:

Strengthen its position as a credible global business hub

Align with international tax transparency standards

Meet OECD and global minimum tax expectations

Support long-term economic sustainability

The aim is not to discourage business — but to create a modern, trusted tax system.

A tax period is the 12-month financial year used by the business for preparing financial statements.

If your financial year runs from 1 July 2023 to 30 June 2024, UAE Corporate Tax applies from 1 July 2023

If your financial year runs from 1 January 2023 to 31 December 2023, Corporate Tax applies from 1 January 2024

Under Article 11, Corporate Tax applies to:

Resident persons, and

Non-resident persons with UAE-sourced business income

Further guidance on taxable persons and income determination is provided in Articles 11 and 20 of the law.

Taxable income is based on the business’s accounting net profit or loss, adjusted for specific items required by the Corporate Tax Law.

Adjustments typically include:

Non-deductible expenses

Exempt income

Reliefs and elections under the law

The starting point is always properly prepared financial statements.

The UAE operates a tiered corporate tax rate system:

0% on taxable income up to AED 375,000

9% on taxable income exceeding AED 375,000

This structure supports small businesses and start-ups while applying a modest rate to larger profits.

If a business has taxable income of AED 500,000:

First AED 375,000 → taxed at 0%

Remaining AED 125,000 → taxed at 9%

Corporate Tax payable:

AED 125,000 × 9% = AED 11,250

Any eligible foreign tax credits may reduce the final tax payable.

Certain entities are fully exempt from UAE Corporate Tax, including:

Government entities

Government-controlled entities

Extractive and non-extractive natural resource businesses (subject to conditions)

Qualifying Public Benefit Entities

Qualifying Investment Funds

Regulated pension and social security funds

UAE entities wholly owned and controlled by exempt persons (subject to criteria)

Additional references are made to Articles 23 and 25.

Even for taxable persons, some income categories are exempt, including:

Dividends and profit distributions from UAE or qualifying foreign participations

Certain capital gains, foreign exchange gains, and impairment gains

Income from foreign branches where a Foreign Permanent Establishment exemption is elected

Income earned by non-residents from international shipping or aviation (subject to conditions)

A group of UAE companies may elect to form a tax group and be treated as a single taxable person, provided conditions are met.

Key conditions include:

Minimum 95% ownership

Neither parent nor subsidiary is an exempt person

Benefits include:

Filing one corporate tax return for the group

Offsetting tax losses between group companies

Detailed rules are set out in Article 40.

Corporate Tax returns must be filed electronically

Filing and payment are due within 9 months of the end of the financial year

Only one return per tax period is required

The UAE Corporate Tax Law introduces arm’s length transfer pricing rules under Article 34.

Related-party transactions must:

Reflect market terms

Be supported by documentation

Align with OECD transfer pricing principles

The FTA may request submission of the financial statements used to determine taxable income.

This highlights the importance of:

IFRS-compliant accounts

Accurate bookkeeping

Clear audit trails

Businesses must retain all Corporate Tax-related records for 7 years from the end of the relevant tax period.

This includes:

Financial statements

Invoices and contracts

Tax computations

Supporting schedules

UAE Corporate Tax is now in force for business profits

It applies across all emirates as a federal tax

Employment income of individuals is not subject to corporate tax

Foreign taxes may be credited against UAE Corporate Tax

The Federal Tax Authority administers and enforces the law

Records must be retained for 7 years

Corporate Tax returns are filed once per financial year, electronically

At Direct Assist, we support UAE businesses with:

✅ Corporate Tax registration and compliance

✅ Tax computations and filings

✅ IFRS-aligned financial statements

✅ Transfer pricing advisory

✅ Group tax structuring

✅ Ongoing bookkeeping and tax planning

👉 Contact Direct Assist today for a free consultation or instant online quote.

Direct Assist – Chartered Certified Accountants helping businesses stay compliant and confident in the UAE.

Excellent rating

Based on 84 reviews

(0203) 633 2018

info@directassistaccountants.co.uk

Provide your details and one of our experts will be in touch.